Life Insurance In Depth

In our Life Insurance 101 blog post we covered the basics of life insurance – what is it, what kinds are there, and how much of it do you need. But with September being NAIFA’s Life Insurance Awareness Month, we’re taking a deeper dive into the kinds of life insurance.

You already know from our 101 post that the kinds of life insurance can be broken down into term insurance and permanent insurance. Term is the simplest, so we’ll begin by shedding light on a few more details of term before going into the more complex topic of permanent insurance.

Term Insurance

To steal (…is it stealing if it’s mine?) the basics from our previous blog post, term insurance is where you pay premiums for a specified period of time (usually anywhere from 10-30 years) and you’re covered under that term as long as premiums are paid. Over the life of the term, your annual premium doesn’t change, nor does your death benefit. At the end of the term, most policies do have the option to continue the coverage but at MUCH higher rates which will continue to increase each year.

Most term policies do have a premium grace period (generally 30 days) where you can pay the premium late and still retain your insurance coverage. If, after the grace period ends, you still want to retain that life insurance policy you’ll typically have to go through a reinstatement process. During reinstatement, your medical history and records are subject to review by the insurance carrier, and you may even be asked to do another medical exam.

Another term insurance concept you may have heard is laddered term insurance. Contrary to how the name may sound, laddered term isn’t a type of policy but rather is a way to structure your term life insurance policies. Because your insurance needs vary over the course of, say, 30 years, you may or may not need as much coverage at certain periods of time.

Let’s pretend we’ve currently determined you need $2 million in life insurance coverage to satisfy your wishes if you were to pass early. This may include things such as paying off the house, setting the kids up for college, ensuring your spouse maintains his/her lifestyle. But in 10 years the house will be paid off, reducing your need by $500,000. Then in another 5 years, both kids will be done with college which reduces your need by another $500,000. All that’s left would be spousal lifestyle maintenance, which again, would decrease overtime as your investments grew.

So using the example above, we would likely structure you with a 10-year policy for $500,000; a 15-year policy for $500,000 and a 20-year policy for $1 million. That way you’re only paying for the coverage you need over the 20-year period. This laddered term structure is usually more cost effective than getting a 20-year $2 million policy, and you’re not paying for insurance you no longer need.

Permanent Insurance

The key to understanding permanent life insurance is to understand the three basic parts that make up the policy. First is death benefit which is the amount you’re “insured” for and is payable upon your death (assuming you’re the insured). Next is the cash value – this is a component that’s not available in term life, but it’s a cash savings component of the policy. Last (for the sake of simplicity) is the premium, which is the amount you pay the insurance company to insure you.

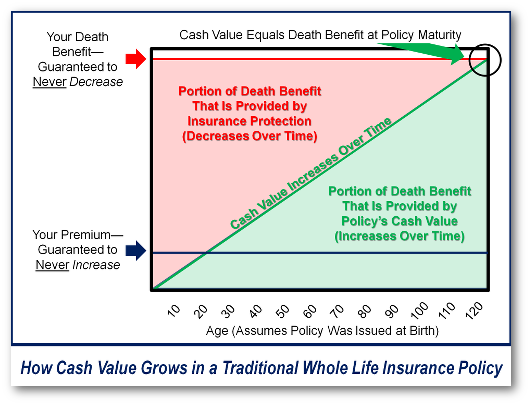

Different forms of permanent insurance can play with these three variables to end up with very different policy structures. For example, a whole life insurance policy is typically where the death benefit and premium stay consistent throughout the life of the policy (commonly to your age 100). And throughout that time period, the cash value increase is a subsequent decrease in the death benefit amount the insurance company must cover (your cash value helps to pay the death benefit). That is how you’re able to pay consistent premiums even as you age and the cost of insuring you goes up. Here’s a great visual depiction of how whole life works.

{kind=link}

A Universal Life (UL) policy has flexibility in both the death benefit and the premium payments. Then other features are added in for additional types of policies, e.g. Variable Universal Life (VUL) or Indexed Universal Life (IUL) policies. A VUL has the flexibility of a UL for premiums and death benefit, and additionally, your cash value component is invested and is subject to the fluctuations of the investment. IULs are like VULs except that the cash value is put into an indexed investment, often with some guarantees on floors and/or ceilings of the investment’s returns.

With the flexibility of ULs, VULs and IULs also comes added layers of complexity. Remember, the insurance companies are for-profit businesses so they only structure policies in a way that makes sense for them. The more variables you’re able to tailor for the insurance to suit your needs, the more complex it will have to be from the carrier’s side of things to ensure they remain profitable. In addition to the 3 basic components, carriers have added a multitude of what they call “rider” options which can be purchased for an amount in addition to the premium, but they come with their own various features and guarantees.

The last type of permanent policies we’re getting into for this post is Survivorship policies, which were once referred to as “second to die” policies. Basically, the policy is on the life of two people instead of one, and the death benefit is paid out on the second death of the insureds. These policies are commonly used for estate and legacy planning; and because it’s on the life of two people, better rates can often be obtained than if insured separately. These survivor policies can take on the properties of ULs, VULs or IULs - for example an SIUL is a Survivorship Indexed Universal Life policy and functions much the same as an IUL but will only payout on the second death.

Never purchase a policy you don’t understand

While life insurance is a valuable component of a well-constructed financial plan, it’s easy to see how complex insurance can get, and very quickly. My number one recommendation with life insurance is and has always been to never purchase a life insurance policy that you don’t understand. With our financial planning software and detailed analyses, we’re able to give several options for how you could utilize life insurance to best reach your goals.

If you’re wondering if your current policy still fits your needs, of if you’re thinking it might be time to get insured, please don’t hesitate to reach out to myself or any one of my team members and we’ll be happy to walk you through the process.